Ledger,Group,Voucher Entery

What is a Ledger?

A Tally Ledger is one of the most important elements in Tally Prime.

It represents an individual account where all the transactions related to a specific item, person, expense, income, asset, or liability are recorded.

Definition:

A Ledger in Tally is a record of all financial transactions related to a particular account.

Every transaction you enter in Tally must be linked to two or more ledgers (as per the double-entry system).

Examples of Ledgers:

- Cash Account

- Bank Account (SBI, HDFC, etc.)

- Sales Account

- Purchase Account

- Capital Account

- Rent Account

- Electricity Expense Account

- Debtors (Customers) – e.g., Rahul Traders

- Creditors (Suppliers) – e.g., ABC Suppliers

Why Ledgers Are Important in Tally?

- Every voucher entry uses ledgers.

- Helps keep accounts organized under proper groups.

- Generates reports like Balance Sheet, P&L, Stock Summary, etc.

- Ensures accurate financial analysis.

Each Ledger Has Two Important Things:

1. Name of the Ledger

(E.g., Cash, Sales, Purchase, Rent, Electricity, etc.)

2. Under (Group)

This shows under which category the ledger belongs, such as:

- Cash-in-hand

- Bank Accounts

- Sales Accounts

- Indirect Expenses

- Sundry Debtors

- Sundry Creditors

Simple Example:

If you create a Rent Account ledger:

- Name: Rent

- Under: Indirect Expenses

Whenever you pay rent, Tally will use this ledger to record the expense.

In Short:

The Tally Ledger is the basic building block of accounting in Tally.

Without ledgers, you cannot record any transactions.

What is a Voucher in Tally Prime?

A Voucher in Tally is a document used to record a transaction.

It is the screen where you enter debit and credit information.

Every financial activity in a business — buying, selling, paying, receiving — is recorded using vouchers.

Why Vouchers Are Important?

- They record every transaction of the business

- They help maintain accurate accounts

- They follow the double-entry system (Debit–Credit)

- They help generate reports like Trial Balance, Profit & Loss, and Balance Sheet

Types of Vouchers in Tally Prime?

Tally provides predefined voucher types for different kinds of transactions.

These vouchers are grouped into Accounting, Inventory, and Order vouchers.

A. Accounting Vouchers

These record financial transactions.

1. Contra Voucher (F4)

Used for cash ↔ bank transfers.

Examples:

- Cash deposited in bank

- Cash withdrawn from bank

2. Payment Voucher (F5)

Used when the business pays money.

Examples:

- Paying salary

- Paying rent

- Paying supplier

3. Receipt Voucher (F6)

Used when the business receives money.

Examples:

- Customer payment

- Interest received

4. Journal Voucher (F7)

Used for adjustment entries (not involving cash or bank).

Examples:

- Depreciation

- Outstanding salary

- Prepaid expenses

5. Sales Voucher (F8)

Used when the business sells goods or services.

Examples:

Selling products to customers

6. Purchase Voucher (F9)

Used when the business buys goods or services.

Examples:

- Purchasing raw materials

- Buying products for resale

7. Debit Note

Issued when goods are returned to the supplier or overcharged.

(Also called Purchase Return)

8. Credit Note

Issued when customer returns goods or is overcharged.

(Also called Sales Return)

B. Inventory Vouchers

Used for stock or product movement.

1. Delivery Note

When goods are sent out to customers.

2. Receipt Note

When goods are received from suppliers.

3. Stock Journal

Used for stock adjustment or stock transfer.

4. Physical Stock

Used for stock verification.

C. Order Vouchers

1. Sales Order

When a customer places an order.

2. Purchase Order

When the business orders goods from a supplier.

Example to Understand Voucher Entry

Transaction: Paid ₹5,000 Rent in Cash

- Voucher Type: Payment Voucher

- Debit: Rent A/c ₹5,000

- Credit: Cash A/c ₹5,000

This is entered in the Payment Voucher screen.

In Short:

- Voucher = Transaction Entry

- Every transaction must be recorded through a voucher

- Different vouchers are used for different activities

What is a Group in Tally Prime?

A Group in Tally is a category used to classify ledger accounts.

Tally uses groups to identify:

- Whether a ledger is an asset, liability, income, or expense

- Where it will appear in the Balance Sheet or Profit & Loss A/c

- How reports should be generated

Every ledger you create must belong to a group.

This is done using the “Under” option while creating a ledger.

Why Groups Are Important?

They help Tally organize accounts properly.

They allow Tally to automatically prepare financial statements.

They ensure accuracy in accounting.

They help in summarizing financial information.

Without groups, ledgers cannot be classified correctly.

Types of Groups in Tally

Tally has 28 predefined groups divided into two main categories:

A. Primary Groups (Balance Sheet Items)

These groups relate to Assets and Liabilities.

1. Capital Account

- Owner’s capital

- Drawings

- Reserves & Surplus

2. Loans (Liability)

- Bank Loan

- Debentures

- Secured & Unsecured Loans

3. Current Liabilities

- Sundry Creditors

- Outstanding Expenses

- Duties & Taxes (GST, VAT)

- Provisions

4. Current Assets

- Cash-in-Hand

- Bank Accounts

- Sundry Debtors

- Stock-in-Hand

- Deposits

- Advance Payments

5. Fixed Assets

- Land & Building

- Furniture

- Machinery

- Vehicles

6. Investments

- Shares

- Mutual Funds

- Bonds

7. Suspense Account

Used temporarily when an account is not identified.

8. Misc. Expenses

Deferred expenses or preliminary expenses.

B. Revenue Groups (Profit & Loss Items)

These groups relate to Incomes and Expenses.

9. Direct Income

- Sales-related income

- Export incentives

10. Indirect Income

- Commission Received

- Interest Received

- Discount Received

11. Direct Expenses

- Wages

- Freight Inwards

- Power & Fuel

- Carriage Inwards

12. Indirect Expenses

- Rent

- Salary

- Advertising

- Electricity

- Telephone

All 28 Groups in Tally (Complete List)?

Primary Groups

Capital Account

Reserves & Surplus

Loans (Liability)

Current Liabilities

Duties & Taxes

Provisions

Bank OD A/c

Secured Loans

Unsecured Loans

Current Assets

Bank Accounts

Cash-in-Hand

Sundry Debtors

Fixed Assets

Investments

Loans & Advances (Asset)

Stock-in-Hand

Deposits (Asset)

Branch/Divisions

Suspense Account

Misc. Expenses (Asset)

Revenue Groups

Sales Accounts

Purchase Accounts

Direct Income

Indirect Income

Direct Expenses

Indirect Expenses

Closing Stock

Simple Example to Understand Groups

Example 1: Creating a Rent Ledger

- Ledger Name: Rent

- Under: Indirect Expenses

Because rent is an expense, it falls under Indirect Expenses.

Example 2: Creating a Customer Ledger

- Ledger Name: Rahul Traders

- Under: Sundry Debtors

Because customers who buy on credit are debtors.

Example 3: Creating a Bank Account Ledger

- Ledger Name: HDFC Bank

- Under: Bank Accounts

Because it is part of your current assets.

In Short

- Group = Category

- Ledger = Account

- Voucher = Transaction

Groups help Tally determine where a ledger appears in the accounting system.

Types of Businesses in Accounting

1. Service Organisation / Service Company

A business that provides services instead of physical products.

Examples:

- Hospitals

- Banks

- Salons

- Hotels

- Transport services

- IT services

Features:

- No inventory

- Revenue from services

- Labour-intensive

Short Answer

Types of companies:

- Service Organisation – provides services

- Trading Company – buys and sells goods

- Manufacturing Company – produces goods

2. Trading Company

A business that buys goods and sells them without changing their form.

Examples:

- Supermarkets

- Clothing stores

- Electronics shops

- Wholesalers

- Retailers

Features:

- Maintains inventory (goods for resale)

- Buys at one price, sells at a higher price

- Profit = Selling Price – Cost Price

3. Manufacturing Company

A business that converts raw materials into finished products.

Examples:

- Furniture factories

- Car manufacturers

- Food processing units

- Textile mills

- Toy factories

Features:

- Uses raw materials, labor, and machines

- Produces finished goods

Has 3 types of inventory:

- Raw materials

- Work-in-progress (WIP)

- Finished goods

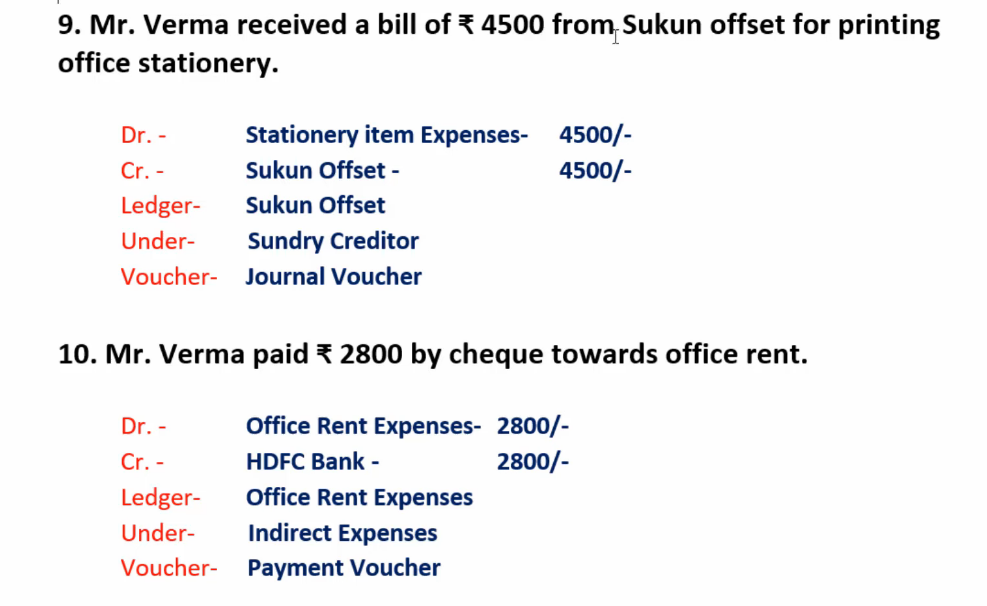

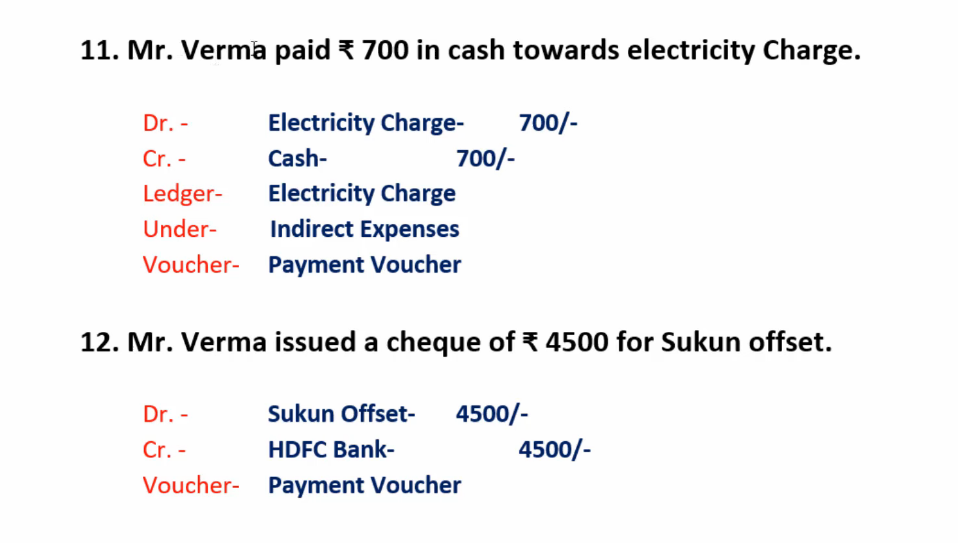

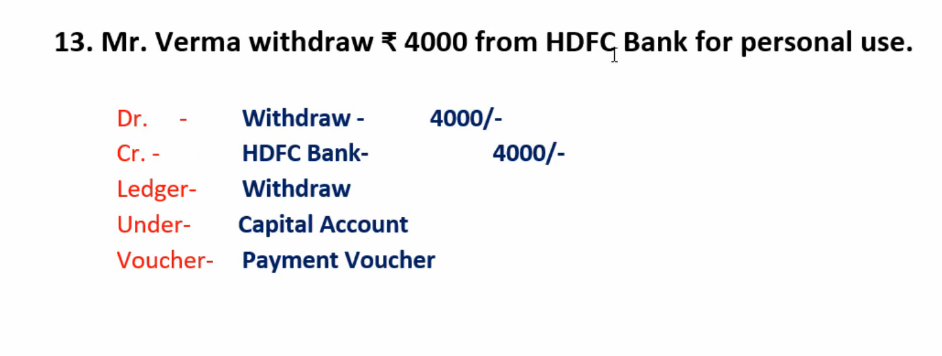

Voucher Entery In Tally

Date:- 1-4-2020

1. Arpit Kumar Verma started a business solutions by bringing in cash of Rs.300000.?

Credit – Arpit Kumar Verma

Debit – Cash

Ledger – Arpit Kumar Verma

Under – Capital account

Voucher – Recipet

Account – Arpit kumar verma,Cash

Golden Rule – (Giver – Arpit kumar verma Credit) (Whats Goes – Cash Debit)

Date:- 2-4-2020

2. Mr. Verma paid Rs.22500 in cash to purchase a computer.The computer does not have any disposal value at the end

Credit – Cash

Debit – Computer

Ledger – Computer

Under – Fixed Assets

Voucher – Payment

Account – Computer,Cash

Golden Rule – (Whats Come – Computer Debit) (Whats Goes – Cash Credit)

Date:- 3-4-2020

3. Mr. Verma opened a bank account in HDFC Bank and deposit cash of Rs.100000

Credit – Cash

Debit – HDFC Bank

Ledger – HDFC Bank,Cash

Under – Bank Account

Voucher – Contra

Account – Personal,Real

Golden Rule – (Whats Goes – Cash Debit) (Giver – Cash Credit)

Date:- 4-4-2020

4. Mr. Verma rented an office apace for Rs.2500 per month on April 01, 2020 He paid the security deposit of Rs. 25000 by cheque.

Credit – HDFC Bank

Debit – Security Deposit

Ledger – Security Deposit,HDFC Bank

Under – Deposits Asset

Voucher – Payment

Account – Nominal,Personal

Golden Rule – (Expence – Security Deposit Debit) (Giver – HDFC bank Credit)

Date:- 5-4-2020

5. Mr. Verma issued cheque and purchased the following fixed assets.

1. Cell Phone Rs.6000 (useful life-5 years)

2. Furniture Rs.20000 (useful life-8 years)

3. AIR Conditioner Rs.20000 (useful life-6 years)

4. Electrical fittings Rs.15000 (useful life-10 years)

The above assets do not have any disposal value at the end

of their useful life.

Credit – HDFC Bank

Debit – Cell Phone,Furniture,AIR Conditioner,Electrical fittings

Ledger – Cell Phone,Furniture,AIR Conditioner,Electrical fittings,HDFC Bank

Under – Indirect Expenses

Voucher – Payment

Account – Real,Personal

Golden Rule – (Expenses – Security Deposit) (Giver – HDFC Bank – Credit)

Date:- 6-4-2020

6. Mr. Verma obtained a mobile phone subscription from Planet telecommunications, by paying a deposit of Rs.3000 in cash.

Credit – Cash

Debit – Security Deposit

Ledger – Security Deposit Phone,Cash

Under – Deposits Asset

Voucher – Payment

Account – Real,Real

Golden Rule – (Whats Come – Security Deposit) (Whats Goes – Cash)

Date:- 20-4-2020

7. Mr. Verma purchased stationary consumables worth Rs.12500 from Global House, on credit.

Credit – Global House

Debit – Stationary

Ledger – Stationary Expenses,Global House

Under – Indirect Expenses,Sundery Creditors

Voucher – Journal

Account – Personal,Nominal

Golden Rule – ( Expenses – Stationary) (Giver – Global House Credit)

8.Date:- 21-4-2020

8. Mr. Verma signed a contract with Silver Services to provide consultancy services at an agreed price of Rs.75000. He received an advance of Rs.25000 by cheque.

Credit – Advance Consultancy

Debit – HDFC Bank

Ledger – Advance Consultancy

Under – Create Secondery Group (Advance From Customar)

Voucher – Recipt

Account – Personal,Real

Golden Rule – ( Reciver – HDFC Bank Debit) (Whats Come – Advance Consultancy Credit)

Date:- 23-4-2020

9. Mr. Verma deposit Rs.50000 cash in HDFC Bank.

Credit – Cash

Debit – HDFC Bank

Ledger – HDFC Bank,Cash

Under – Bank Account

Voucher – Contra

Account – Personal,Real

Golden Rule – ( Reciver – HDFC Bank Debit) (Whats Goes – Cash Credit)

Date:- 25-4-2020

10. Mr. Verma received an invoice for Rs.6000 from Ink and Paper Publishers for printing office stationary.

Credit – Ink and Paper Publishers

Debit – office stationary

Ledger – Ink and Paper Publishers,Stationary

Under – Sundery Creditor,Indirect Expences

Voucher – Journal

Account – Personal,Nominal Account

Golden Rule – (Giver – Ink and Paper Publishers – Credit) (Expence – Stationary Debit)

Date:- 27-4-2020

11. Mr. Verma withdrew Rs.7500 cash for personal use.

Credit – Cash

Debit – withdrew

Ledger – Cash,Withdrew

Under – Capital Account

Voucher – Payment

Account – Personal,Nominal Account

Golden Rule – ( Giver – Bussines – Credit) ( withdrew – Debit)

Date:- 30-4-2020

Mr. Verma paid Rs.750 in cash towards office maintenance charges.

Credit – Cash

Debit – office maintenance

Ledger – office maintenance,Cash,

Under – Indirect Expences,

Voucher – Payment

Account – Real,Nominal Account

Golden Rule – (What Goes – Cash – Credit) (Expences – office maintenance – Debit)