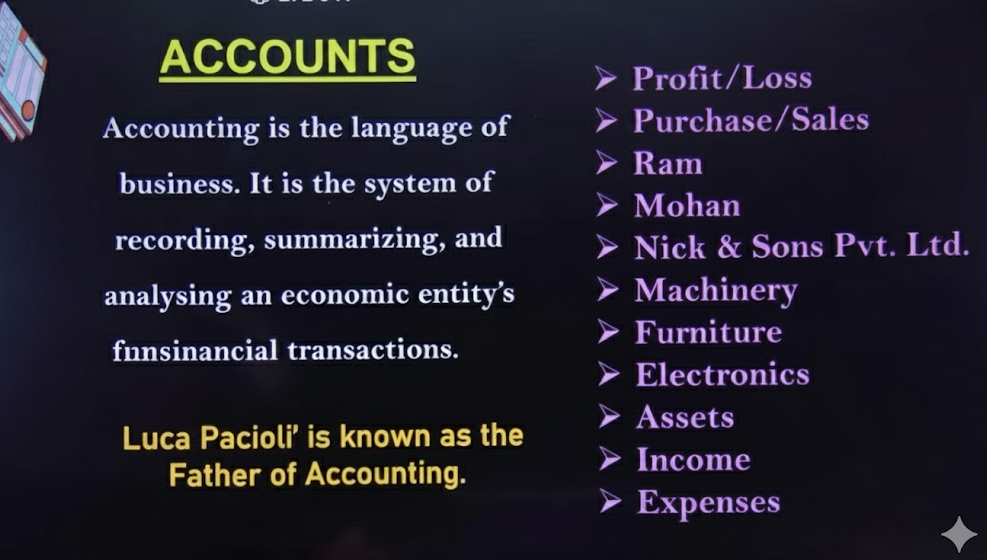

What Is Accounting?

Accounting is the process of recording, classifying, summarizing, and interpreting financial transactions of a business.

It helps businesses:

- Know their financial position

- Track income and expenses

- Make informed decisions

- Comply with legal and tax requirements

In simple words: Accounting is the language of business.

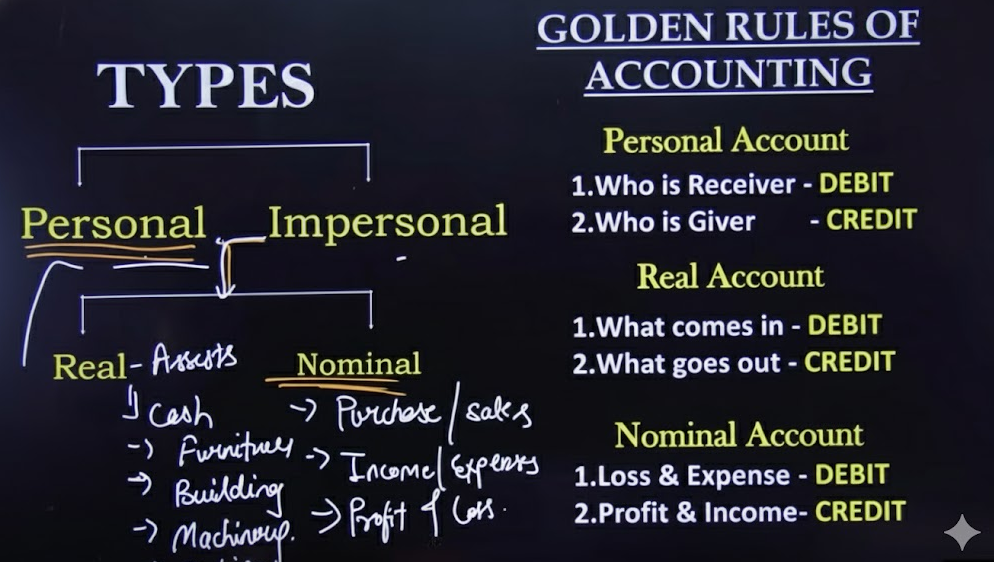

Types of Accounts in Accounting?

Accounting uses the Double-Entry System, where every transaction affects two accounts.

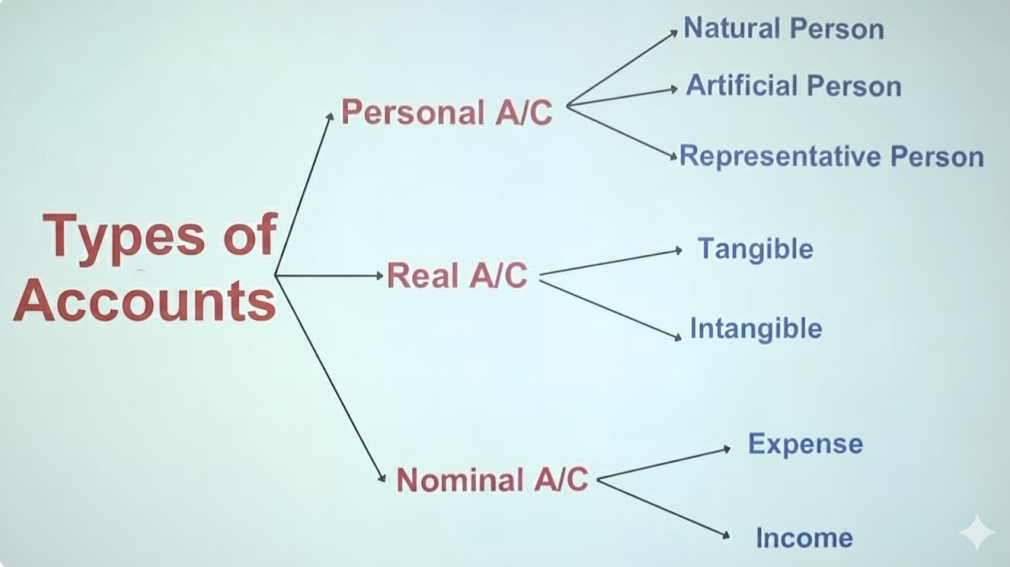

There are 5 main types (or categories) of accounts:

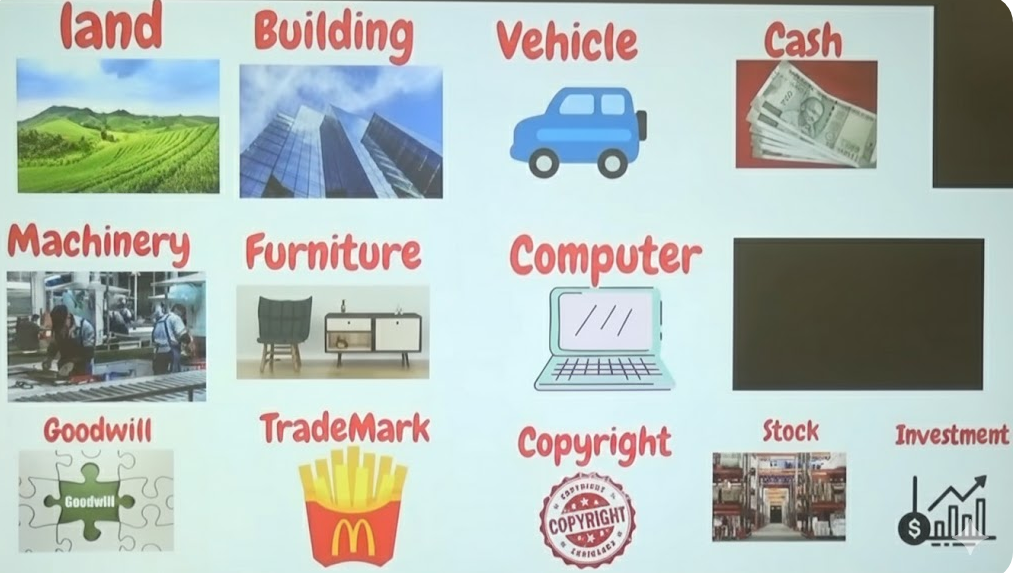

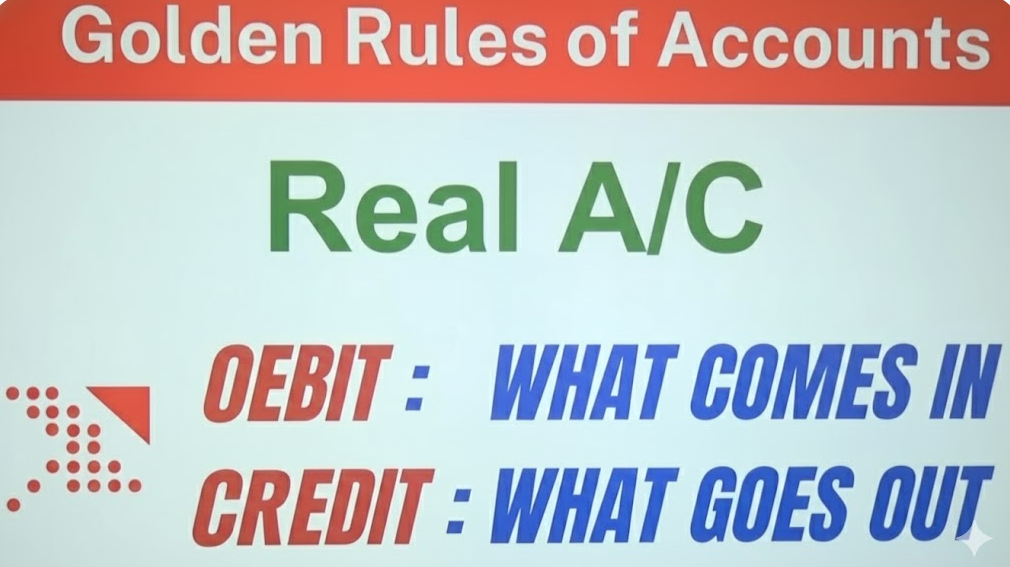

1 Assets

Assets are resources owned by a business.

Examples:

- Cash

- Machinery

- Buildings

- Inventory

- Accounts Receivable

Rule:

- Debit increases assets

- Credit decreases assets

2 Liabilities

Liabilities are the obligations or debts of a business.

Examples:

- Loans

- Accounts Payable

- Outstanding Expenses

- Bank Overdraft

Rule:

- Credit increases liabilities

- Debit decreases liabilities

3 Equity (Capital)

Equity represents the owner’s interest in the business.

Examples:

- Capital

- Drawings (withdrawals reduce capital)

- Retained earnings

Rule:

- Credit increases equity

- Debit decreases equity

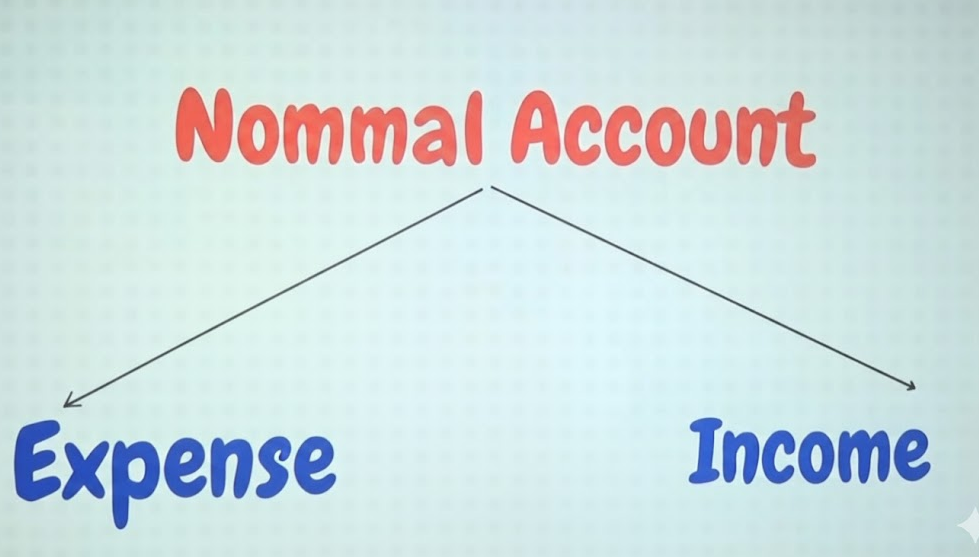

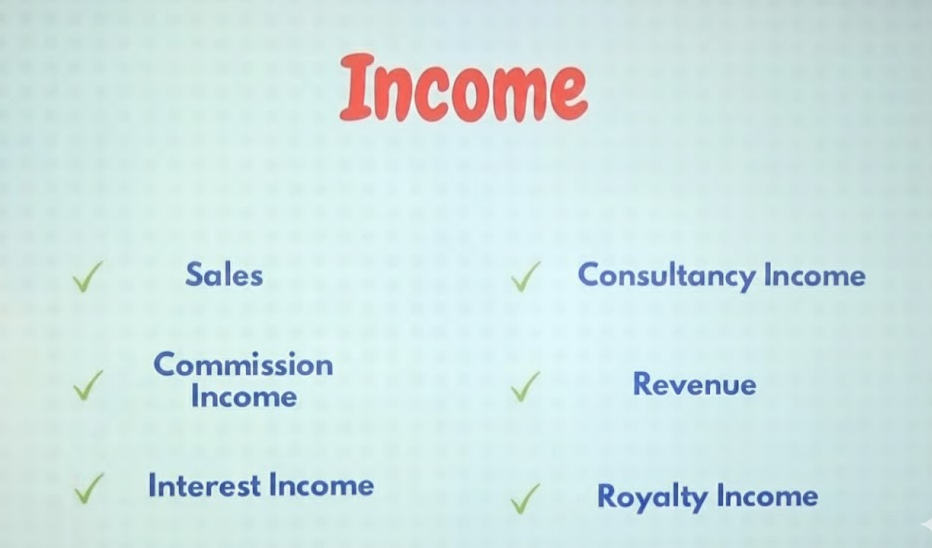

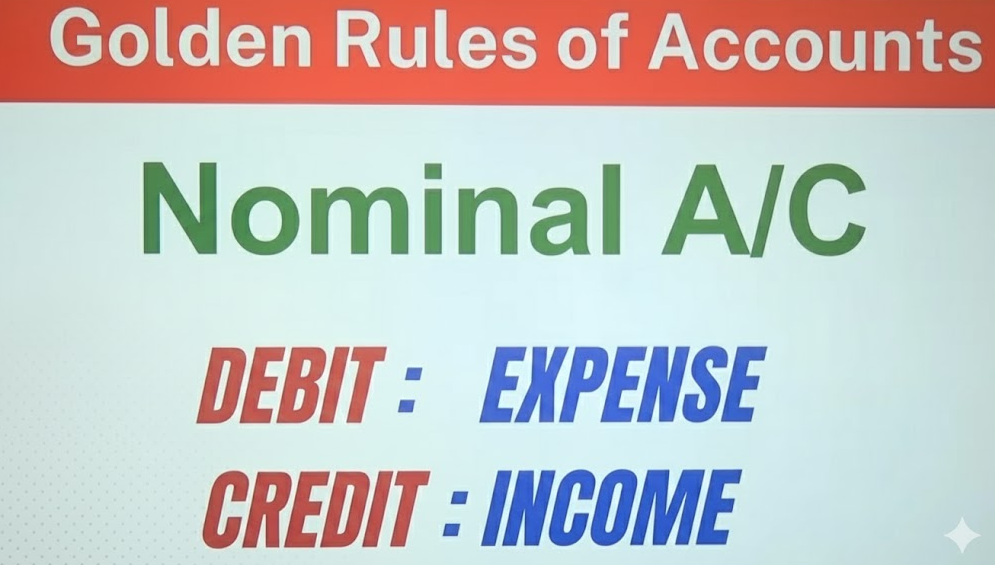

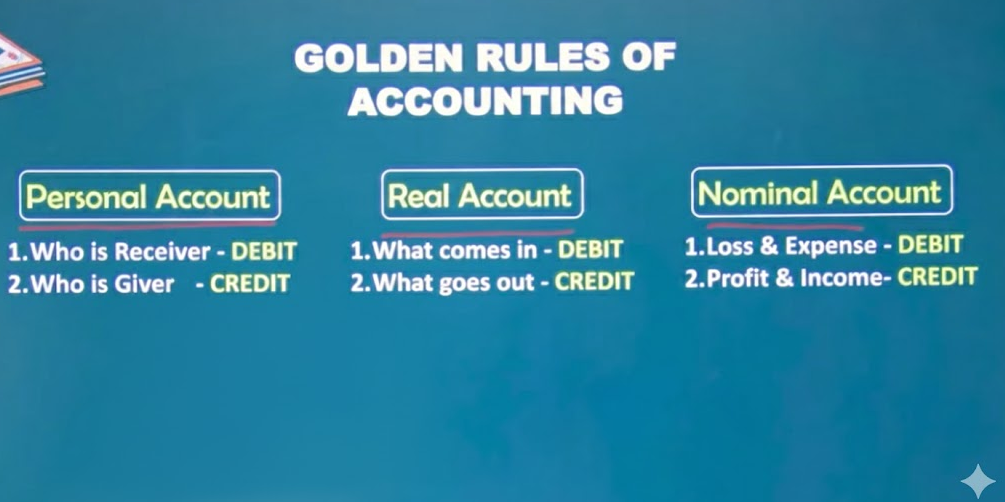

3 Income (Revenue)

Income is what the business earns.

Examples:

- Sales

- Service income

- Interest income

Rule:

- Credit increases income

- Debit decreases income

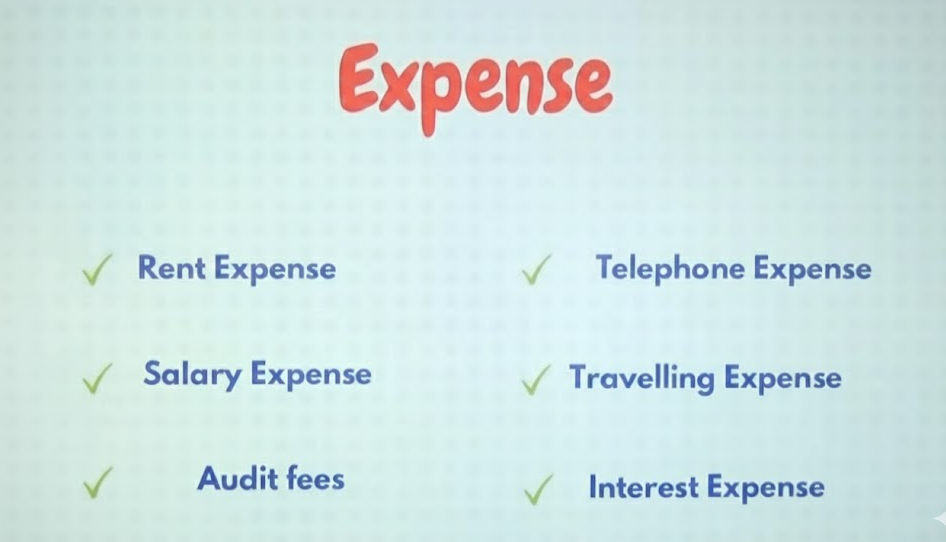

4 Expenses

Expenses are costs incurred to run the business.

Examples:

- Rent

- Salaries

- Electricity

- Stationery

- Advertising

Rule:

- Debit increases expenses

- Credit decreases expenses

Key Functions of Accounting?

- Records transactions (like sales, purchases, expenses)

- Classifies them into categories

- Summarizes them into reports (like balance sheet, income statement)

- Analyzes financial performance

- Helps in decision-making

- Ensures legal compliance (taxes, audits, etc.)

Why Accounting Is Important?

- Shows profit or loss

- Helps track business growth

- Controls expenses

- Helps attract investors

- Provides information for planning and budgeting

Simple Definition in Accounting?

Accounting is the systematic process of keeping financial records so that a business can understand its financial position and make informed decisions.

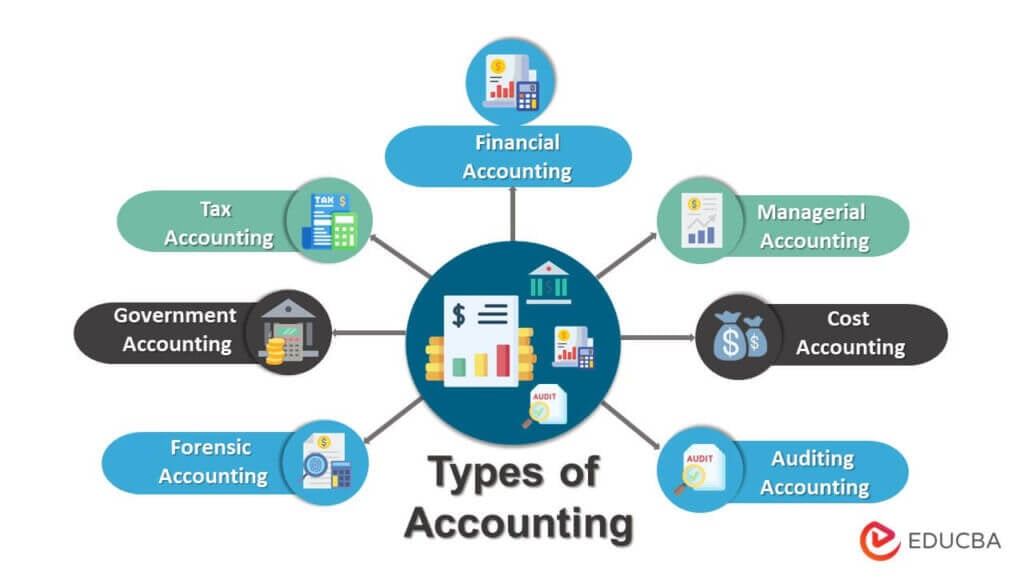

Types of Accounting?

1 Financial Accounting

Focuses on preparing financial statements for external users like investors, banks, and government.

Includes:

- Balance Sheet

- Income Statement

- Cash Flow Statement

Purpose: Shows financial performance and position.

2 Management Accounting

Provides financial information to internal users (managers) for decision-making.

Covers:

- Budgeting

- Cost control

- Performance evaluation

Purpose: Helps managers plan and make strategic decisions.

3 Cost Accounting

Deals with calculating the cost of producing goods or services.

Includes:

- Material cost

- Labor cost

- Overheads

Purpose: Helps control costs and set product prices.

4 Tax Accounting

Focuses on preparing and filing tax returns and ensuring tax compliance.

Includes:

- Income tax

- GST/VAT

- Tax planning

Purpose: Follows tax laws and reduces tax liability legally.

5 Auditing

Examines the accuracy of financial records and statements.

Types:

- Internal audit

- External audit

Purpose: Ensures financial reliability and prevents fraud

6 Forensic Accounting

Investigates financial fraud, embezzlement, and disputes.

Used by:

- Police

- Courts

- Insurance companies

7 Government Accounting

- Used in government departments to record public funds, budgets, and expenditures.

8 Project Accounting

- Used to track the financial progress of specific projects.

Used in:

- Construction

- Engineering

- IT projects